TL;DR:

- Many high earners relocating from California or New York can save thousands annually by moving to no-income-tax states, but family priorities often extend beyond tax savings.

- Understanding personal motivations, such as family ties, job opportunities, and lifestyle, is essential for making informed relocation decisions in 2026.

Families earning $200,000 or more in California or New York can save between $18,000 and $133,000 annually simply by relocating to a no-income-tax state. That number stops people cold, and it should. But the real story behind the 2026 migration wave is far more layered than a single tax calculation. Millions of homeowners and families are rethinking where they live, and the reasons stretch well beyond what shows up on a tax return. This guide breaks down every major factor, the real tradeoffs, and the practical steps you need to make a confident decision.

Table of Contents

- Beyond taxes: The core reasons Americans move in 2026

- How cost savings compare across popular relocation routes

- Risks, roadblocks, and new realities: What to watch in 2026

- Next steps: Making an informed, stress-free move

- What most relocation guides miss about leaving high-cost states

- Simplify your relocation with trusted moving experts

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Multiple motivations | Americans are moving for a mix of family, jobs, lifestyle, and taxes—not just one reason. |

| Substantial savings possible | Moving from high-cost to affordable states can yield up to $133,000 in yearly savings. |

| New relocation risks | Consider mortgage lock-in, tax audits, and crowded destinations when making your move. |

| Mid-size cities rising | Knoxville, Boise, and similar markets are the hot relocation targets for families in 2026. |

| Smart planning pays off | Thorough preparation and professional help make interstate moves far less stressful. |

Beyond taxes: The core reasons Americans move in 2026

Understanding the headline numbers only tells part of the story. It’s crucial to unpack what really tips the scales for today’s movers before you start packing boxes or calling moving companies.

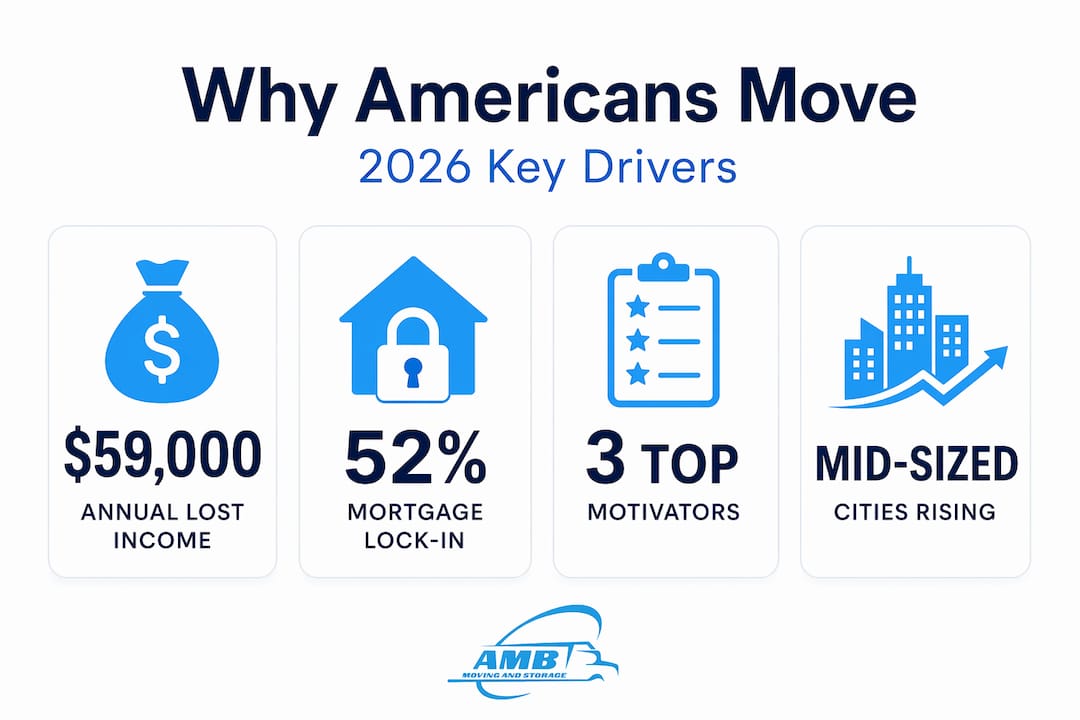

Most people assume taxes are the single biggest driver of interstate migration. The data says otherwise. Taxes explain roughly 11% of migration decisions overall, though their weight rises sharply among high earners. For the average family, the decision to move is far more personal than financial.

What surveys consistently show about why people move:

- Family ties and proximity to relatives rank as the number one reason people choose a new state

- Job opportunities and career growth come in a close second, especially in remote-work-friendly cities

- Lifestyle changes, including climate, outdoor access, and pace of life, rank third

- Cost of living and taxes rank fourth, though they carry more weight for households earning above $150,000

- Housing affordability has surged in importance since 2022, now closely tied with lifestyle as a motivating factor

This matters because it reframes the entire conversation. If you’re a family of four in the Bay Area spending $5,500 a month on a three-bedroom rental, your move to Boise or Knoxville isn’t primarily about escaping California’s 13.3% top marginal income tax rate. It’s about getting your kids into a yard, cutting your commute, and feeling financially stable again.

That said, high earners tell a different story. California loses an average of $59,000 in adjusted gross income per departing resident, and New York loses $62,000. These are not average workers. They are business owners, tech executives, and investors who are acutely aware of what state taxes cost them. For this group, taxes are a primary driver, not an afterthought.

Understanding the moving cost factors involved in leaving a high-cost state helps you see the full financial picture, not just the tax savings. And tracking 2026 migration shifts shows you where the demand is going, which matters if you plan to sell a home in a competitive market.

| Migration motivator | Share of movers citing it | Higher weight for high earners? |

|---|---|---|

| Family and relationships | 35% | No |

| Job or career opportunity | 28% | Yes |

| Lifestyle and climate | 18% | Yes |

| Taxes and cost of living | 11% | Strongly yes |

| Housing affordability | 8% | Mixed |

How cost savings compare across popular relocation routes

Once you understand the broader motivations, it’s essential to see just how much families can gain in their bank accounts and lifestyles with a relocation. The numbers are striking, and they go beyond just income tax.

Moving from California to Idaho, one of the most popular routes in recent years, can save a household between $30,000 and $40,000 per year. That figure accounts for lower housing costs, reduced state income taxes, cheaper groceries, lower utility bills, and reduced property taxes. For a family earning $120,000, that’s a 25% to 33% increase in effective purchasing power. That’s not a rounding error. That’s a second income.

Savings breakdown for a typical family earning $120,000:

- State income tax savings (CA to ID): $4,000 to $7,000 per year

- Housing cost reduction (own vs. rent): $12,000 to $18,000 per year

- Lower grocery and utility costs: $3,000 to $5,000 per year

- Reduced transportation and insurance costs: $2,000 to $4,000 per year

The New York to Florida route tells a similar story. Florida has no state income tax, and housing costs in cities like Jacksonville or Tallahassee can be 40% to 60% lower than comparable neighborhoods in the New York metro area. A family leaving a $3,800 per month apartment in Brooklyn for a $1,900 per month home in the Tampa suburbs is effectively giving themselves a $22,800 annual raise before touching a single tax form.

Pro Tip: Calculate your personal “relocation breakeven” before committing. Add up your total first-year moving costs, including professional movers, temporary storage, and any overlap in housing payments, then divide by your projected monthly savings in the new state. Most families break even within 6 to 14 months.

One underappreciated obstacle is mortgage lock-in syndrome. Over 52% of American homeowners currently hold mortgage rates below 4%, many locked in during 2020 and 2021. Selling and buying in a new state means taking on today’s rates, which sit considerably higher. This creates a genuine financial friction that keeps many families in place even when the long-term math clearly favors moving.

However, the families who run the full 5 and 10 year projections often find that the cumulative savings in taxes, housing, and cost of living outpace the mortgage rate penalty within a few years. The key is doing the math honestly rather than using the rate lock as an excuse to avoid a decision.

Review 2026 interstate moving costs by route before finalizing your budget, and dig into interstate cost details to understand what variables affect your specific move.

| Route | Avg. annual savings | Primary savings source | Mortgage lock-in risk |

|---|---|---|---|

| California to Idaho | $30,000 to $40,000 | Housing + taxes | Moderate |

| New York to Florida | $25,000 to $45,000 | Taxes + housing | High |

| Illinois to Tennessee | $18,000 to $30,000 | Taxes + cost of living | Moderate |

| Washington to Nevada | $12,000 to $22,000 | Income tax elimination | Low to moderate |

Risks, roadblocks, and new realities: What to watch in 2026

Big rewards come with real risks. The current migration landscape has challenges that didn’t exist a few years ago, and ignoring them can turn a smart financial move into a costly mistake.

Four major risks every relocating family should plan for:

-

State tax audits. California and New York aggressively audit high earners who claim to have changed residency. If you earn significant income and move out of either state, expect scrutiny. You’ll need to document your new domicile thoroughly, including voter registration, driver’s license, bank accounts, and physical presence records. This is not a scare tactic. It’s a real process that catches people off guard every year.

-

Mortgage rate shock. As noted above, 52% of homeowners face mortgage lock-in, and the jump from a 3.2% to a 6.8% rate on a comparable home can add $1,200 to $1,800 per month to your housing payment. This can significantly reduce or eliminate the savings you expected from the move.

-

Saturated destination markets. Sun Belt states like Florida and Texas are now considered “balanced” markets, meaning home prices have risen substantially due to years of migration inflows. The affordability advantage that made Austin or Miami attractive in 2019 has narrowed considerably. Buyers arriving now may find themselves paying near-coastal prices in cities they expected to be bargains.

-

Infrastructure and service gaps. Mid-sized cities absorbing rapid population growth often struggle to keep up with demand for schools, healthcare, and roads. Moving to a fast-growing suburb can mean longer waits for services you took for granted in a larger metro.

“The cities gaining the most attention in 2026 are not the obvious ones. Knoxville, Boise, Huntsville, and Greenville are pulling in families who looked at Austin or Phoenix and found the affordability window had already closed.”

Smart movers are looking beyond the headline destinations. Mid-sized cities in Tennessee, Idaho, Alabama, and South Carolina offer the affordability that Florida and Texas once promised, without the price inflation that comes from being on every relocation blog’s top-ten list.

Review state-to-state moving tips to understand the logistical and legal requirements specific to your route. For cost-conscious families, exploring container cost-saving options can meaningfully reduce your upfront moving expenses.

Pro Tip: Before choosing your destination city, look at its 5-year population growth rate. Cities growing faster than 3% annually often see housing prices and rental costs rise quickly. A city growing at 1% to 2% may offer better long-term affordability stability.

Next steps: Making an informed, stress-free move

Armed with the latest realities and what to watch for, you can take control of your own relocation process. The families who move successfully in 2026 are the ones who treat this like a project with clear phases, not a single impulsive decision.

Your relocation planning checklist:

- Run your breakeven analysis at least 6 months before your target move date. Include moving costs, temporary housing, and any rate differential on a new mortgage

- Consult a tax professional familiar with both your origin and destination states, especially if you earn above $100,000 or have business income

- Research destination neighborhoods beyond the city level. School ratings, commute times, and local property tax rates vary enormously within the same metro area

- Get multiple moving quotes from licensed, insured interstate movers at least 8 to 10 weeks before your move date

- Establish new state residency quickly. Get your new driver’s license, register to vote, and open a local bank account within 30 days of arriving to support your domicile claim

Mortgage lock-in affects over half of homeowners with low rates, but the families who move successfully are the ones who weigh the full picture, not just the monthly payment. A $1,200 increase in mortgage costs can still result in a net gain of $2,000 to $3,000 per month when you factor in tax savings, lower insurance, and reduced cost of living.

| Planning phase | Timeline | Key action |

|---|---|---|

| Research and analysis | 6 to 12 months out | Breakeven calculation, destination shortlist |

| Financial preparation | 4 to 6 months out | Tax consultation, mortgage pre-approval |

| Logistics planning | 2 to 3 months out | Moving quotes, storage arrangements |

| Residency establishment | First 30 days after arrival | License, voter registration, bank accounts |

| Tax documentation | First full year | Track days in each state, save all records |

Follow a step-by-step moving guide designed specifically for families making interstate moves in 2026. For families with large households or staging needs, exploring shipping container savings can reduce the cost of moving bulky furniture and appliances significantly.

What most relocation guides miss about leaving high-cost states

Every guide you’ll read, including this one, gives you tables, checklists, and savings projections. What they rarely address is the emotional weight of the decision, and that weight is often what keeps families stuck.

We’ve worked with thousands of families on long-distance moves, and the pattern is consistent. The financial case for leaving California or New York is often clear within an hour of honest number-crunching. What takes months is the internal negotiation. The question isn’t usually “can we afford to move?” It’s “can we afford to leave our community, our routines, and our sense of identity?”

This is not a soft observation. It’s a practical one. Families who underestimate the social and emotional adjustment after a major move are more likely to experience “mover’s remorse” within the first year. They may return to their origin state, negating all the financial gains and paying moving costs twice.

The families who thrive after long-distance moves share a few traits. They invest time before the move in building connections in the new city, attending local events, joining neighborhood groups, and identifying community anchors like schools, churches, or sports leagues. They treat the social infrastructure of their new home as seriously as the financial one.

There’s also a category of people who stay in high-cost states not because they’ve done the math and decided to stay, but because the decision feels too large to make. Inertia is powerful. The most expensive move destinations in the country are also the ones with the highest rates of long-term residents who have simply never seriously evaluated leaving.

The honest truth is that for many families, the financial case for moving is strong and getting stronger. But the decision to move is ultimately about more than money. It’s about what kind of life you want to build, and whether the place you currently live supports that vision. The families who answer that question clearly, whatever the answer, tend to make better decisions than those who avoid asking it at all.

Simplify your relocation with trusted moving experts

When you’re ready to move from research to action, experienced help makes all the difference between a smooth transition and a stressful one.

Planning a move across state lines involves far more complexity than a local move. Licensing requirements, weight-based pricing, storage coordination, and interstate regulations all add layers that trip up families who try to manage everything independently. AMB Moving & Storage Inc. specializes in exactly these scenarios. Whether you need full-service interstate moving services or the flexibility of long distance moving experts who understand your timeline, our team handles the logistics so you can focus on your family. We also offer storage for families in transition, giving you the flexibility you need when closing dates don’t align perfectly.

Frequently asked questions

How do state taxes affect my annual savings if I move in 2026?

Moving from a high-tax to a no-income-tax state can raise your annual savings by $18,000 to $133,000 depending on your income level, with the largest gains going to high earners leaving California or New York.

What’s the biggest risk for homeowners relocating from California or New York?

High-income earners face the highest audit risk from state tax boards after moving, making thorough residency documentation essential from day one.

Is the Sun Belt still the top destination for movers in 2026?

Florida and Texas are now balanced markets with rising prices, pushing many movers toward mid-sized alternatives like Knoxville, Boise, and Huntsville for better affordability.

How does mortgage lock-in influence whether to move in 2026?

Over half of American homeowners hold low locked-in rates, but 52% still weigh moving when total annual savings of $30,000 to $40,000 and lifestyle improvements outpace the rate increase cost.

What are the best steps for planning a long-distance move from a high-cost state?

Start with a full breakeven analysis, consult a tax professional familiar with both states, compare quotes from licensed interstate movers, and establish new state residency within 30 days of arriving to protect your domicile claim.