TL;DR:

- Federal law requires interstate movers to offer two valuation options: Released Value Protection and Full Value Protection, which differ in payout and cost. Documentation before, during, and after the move is essential for successful claims, with photographs and detailed notes protecting your rights. For high-value items or long-distance moves, Full Value Protection or third-party insurance provides better financial security than the default valuation coverage.

Moving insurance interstate refers to the federally mandated valuation coverage options that protect your household goods when you relocate across state lines. Under U.S. federal law, every licensed interstate mover must offer two distinct protection levels: Released Value Protection and Full Value Protection. These are not optional add-ons. They are legal requirements governed by the Federal Motor Carrier Safety Administration (FMCSA). Knowing the difference between these options, and understanding when third-party moving insurance fills the gaps, is the single most important financial decision you make before moving day.

What are Released Value and Full Value Protection in interstate moving coverage?

Federal law mandates that every interstate mover offer both Released Value Protection and Full Value Protection. These two options define the outer limits of what a mover will pay if your belongings are lost or damaged in transit. Most people default to the free option without reading the fine print, and that decision costs them.

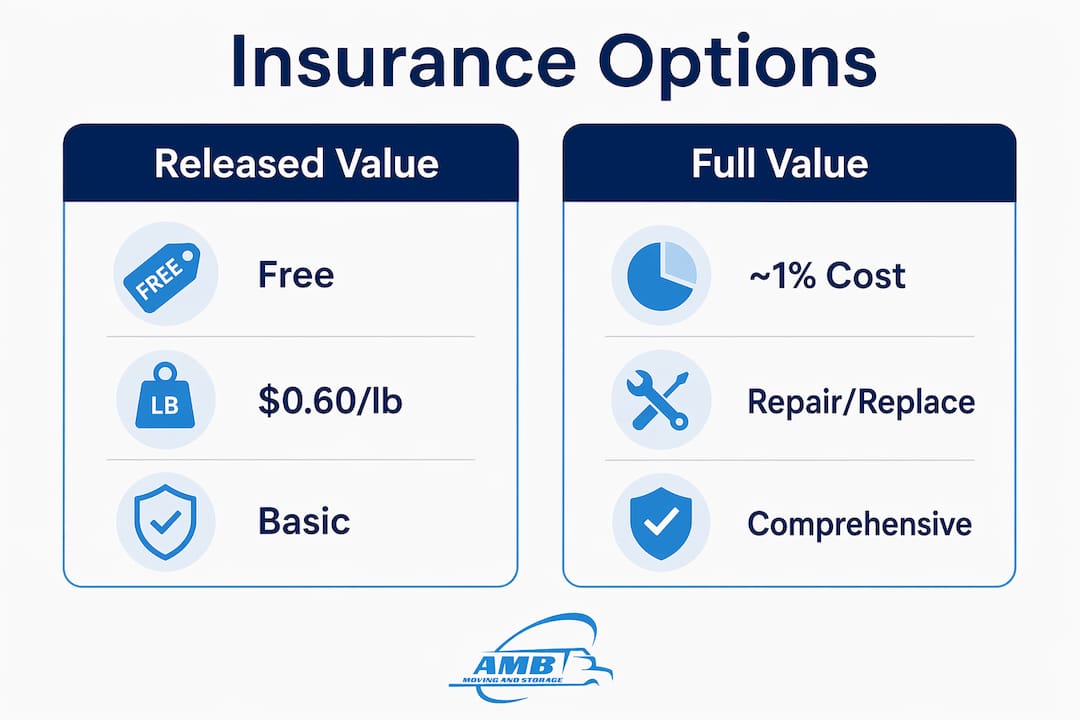

Released Value Protection: the default that often falls short

Released Value Protection is free, but it pays only $0.60 per pound per item. That rate sounds reasonable until you apply it to real items. A 50-pound flat-screen television worth $800 would receive just $30 under this formula. That gap between payout and replacement cost is where most post-move financial pain originates. This coverage level is appropriate only if you are moving low-value, heavy items where replacement cost is genuinely low.

Full Value Protection: the upgrade worth considering

Full Value Protection ties the mover’s liability to the actual repair or replacement cost of damaged or lost items, up to your declared shipment value. Full Value Protection costs roughly 1% of the declared value, though deductibles and minimum declared values vary by mover. For a shipment declared at $50,000, expect to pay approximately $500 for this coverage. That cost provides real financial security for electronics, antiques, artwork, and other items where weight bears no relationship to value.

| Feature | Released Value Protection | Full Value Protection |

|---|---|---|

| Cost | Free | ~1% of declared value |

| Payout basis | $0.60 per pound per item | Repair, replace, or reimburse |

| Best for | Low-value, heavy items | High-value or long-distance moves |

| Deductible | None | Varies by mover |

| Federal requirement | Yes (default) | Yes (must be offered) |

Pro Tip: Before signing any moving contract, ask your mover for the minimum declared value they require for Full Value Protection. Some companies set this floor at $6 per pound of total shipment weight, which may still undervalue a household with high-end electronics or jewelry.

How does valuation coverage differ from traditional moving insurance?

Valuation coverage is not traditional insurance. This distinction matters more than most people realize. Mover’s valuation coverage is a contractual liability the moving company assumes under federal transportation law. It is not regulated by state insurance departments, and it does not function like a homeowner’s or renter’s policy. Moving contracts use valuation language, meaning coverage caps and formulas govern maximum recovery rather than standard insurance principles.

Third-party moving insurance, by contrast, is a standalone policy sold by licensed insurers. It is regulated by your state’s department of insurance and can cover perils that valuation coverage excludes entirely, such as flooding, earthquake damage during transit, or items damaged while in storage. For anyone moving rare instruments, fine art, or irreplaceable heirlooms, a third-party policy is worth the additional premium.

Here are the key factors to weigh when deciding whether to add third-party long distance moving insurance:

- Coverage perils: Valuation covers carrier negligence. Third-party policies can cover Acts of God, theft, and accidental breakage regardless of fault.

- Deductibles: Third-party policies carry deductibles that vary widely. Compare these against the mover’s Full Value deductible before purchasing.

- Storage periods: If your goods will sit in a warehouse between pickup and delivery, confirm whether valuation coverage extends to that period. Many policies do not.

- Exclusions: Both valuation and third-party policies typically exclude items packed by the owner. Professional packing by the mover strengthens your claim position.

- Claims process: Third-party insurers follow state insurance regulations, which often include mandated response timelines and dispute resolution processes.

Pro Tip: Check your existing homeowner’s or renter’s insurance policy before purchasing any supplemental coverage. Some policies provide limited moving coverage, but most exclude transit and storage periods or cap payouts well below replacement value. A five-minute call to your insurer before moving day can save you from paying for duplicate coverage.

What are best practices for documenting and filing claims on interstate moves?

The difference between a successful claim and a denied one almost always comes down to documentation. Instant documentation, including photos and detailed exception notes, is the deciding factor in claim outcomes. Carriers routinely deny claims when shippers cannot prove damage occurred during transit rather than before pickup or after delivery.

Follow these steps to protect your claim rights from the moment your goods are loaded:

- Inspect every item at pickup. Walk through your home with the mover’s inventory list and note the pre-existing condition of all high-value items. Photograph scratches, dents, and wear before anything is wrapped or loaded.

- Review the Bill of Lading before signing. The Bill of Lading is your legal contract. Noting exceptions on the Bill of Lading at pickup and delivery is the foundation of any successful freight claim. Never sign a clean Bill of Lading if you have concerns.

- Inspect at delivery before the movers leave. Open boxes, check furniture, and note any visible damage on the Proof of Delivery form. Do not let time pressure push you into signing without looking.

- Report concealed damage within five days. If you discover damage after the movers have left, written notice within five days of delivery preserves your claim rights for concealed damage. Waiting longer weakens your position significantly.

- File your formal claim within nine months. Under the Carmack Amendment, freight claims must be filed in writing within nine months of delivery. Include a specific dollar amount and all supporting evidence: photos, original purchase receipts, repair estimates, and your exception notes.

- Follow up in writing. Every communication with the mover about your claim should be in writing. Email creates a timestamped record that protects you if the dispute escalates.

A clear paper trail including photos and exception notes significantly improves claim success rates. Carriers may deny claims outright without evidence that damage occurred during transit, so treat documentation as non-negotiable from day one.

How to choose the right moving insurance coverage for your interstate move

Choosing the right interstate moving coverage starts with an honest inventory of what you own and what it would cost to replace. Most people significantly underestimate the total replacement value of their household goods, which leads them to underinsure and absorb preventable losses.

Work through these decision factors before committing to a coverage level:

- Declared value: Calculate the total replacement cost of your shipment, not the sentimental or purchase value. Use current retail prices for electronics, appliances, and furniture.

- Item types: Lightweight, high-value items (laptops, jewelry, cameras) are most exposed under Released Value Protection. These items alone may justify upgrading to Full Value Protection.

- Move distance: Longer routes mean more handling, more transfer points, and statistically more opportunity for damage. Full Value Protection is recommended for high-value or long-distance moves precisely because risk accumulates with distance.

- Risk tolerance: If a total loss would create serious financial hardship, Full Value Protection or a third-party policy is the rational choice. If your belongings are older and easily replaced, Released Value may be acceptable.

When vetting movers, ask these specific questions before signing anything:

- What is your minimum declared value for Full Value Protection?

- What deductible options do you offer?

- Do you extend valuation coverage to storage periods?

- Are owner-packed boxes excluded from your liability?

- What is your average claim resolution timeline?

Pro Tip: Verify any mover’s FMCSA license and insurance status before booking. Use the FMCSA mover verification process to confirm their USDOT number, operating authority, and complaint history. A mover without proper credentials cannot legally offer compliant valuation coverage.

Choosing between coverage levels is ultimately a cost-benefit calculation. Released Value costs nothing but exposes you to significant underinsurance. Full Value Protection costs roughly 1% of declared value and provides real protection. Third-party insurance adds a layer of coverage for perils neither valuation option addresses. For most interstate moves involving a full household, Full Value Protection represents the best balance of cost and protection.

Key takeaways

Choosing the right moving insurance for an interstate move requires understanding that federal law mandates two valuation options, and that neither replaces the broader protection a third-party insurance policy can provide.

| Point | Details |

|---|---|

| Released Value is the default | It pays only $0.60 per pound per item, which severely underinsures lightweight, high-value goods. |

| Full Value Protection costs ~1% | This upgrade ties mover liability to actual repair or replacement cost, not weight. |

| Valuation is not insurance | It is a contractual liability under federal law, not a state-regulated insurance product. |

| Document everything immediately | Photos and Bill of Lading exceptions are the deciding factor in successful damage claims. |

| File claims within nine months | The Carmack Amendment sets a nine-month window; earlier filing produces better outcomes. |

What we’ve learned from years of interstate moves

After handling thousands of interstate relocations, the pattern is consistent: most people who end up disappointed after a move made one of two mistakes. They accepted Released Value Protection without understanding what $0.60 per pound actually means in practice, or they failed to document their belongings before loading began.

The second mistake is the more painful one, because documentation costs nothing. A 20-minute walkthrough with your phone camera before the truck is loaded is the single highest-return action you can take to protect yourself. We have seen claims for thousands of dollars denied because the shipper could not prove the damage did not exist before pickup. That is a preventable outcome.

On the coverage side, the conventional wisdom that “movers are careful so you don’t need Full Value” misses the point. Damage during interstate moves is rarely caused by carelessness alone. Long-haul trucks encounter road vibration, temperature changes, and multiple transfer points. A well-packed box can still arrive with a cracked screen inside. Full Value Protection is not a vote of no confidence in your mover. It is a recognition that transit over hundreds of miles carries inherent risk.

The cost of Full Value Protection is almost always less than the deductible on a homeowner’s policy, and it covers the specific perils of transit that most home policies exclude. For anyone moving a full household across state lines, it is the rational default, not the premium option.

— AMB

Move with confidence: get a quote from Ambmovingservices

Ambmovingservices operates as a fully licensed and FMCSA-compliant interstate moving company with experience across thousands of long-distance relocations nationwide. Every move we handle includes a clear explanation of your valuation coverage options, transparent pricing for Full Value Protection, and guidance on when third-party insurance makes sense for your specific shipment. Our team helps you calculate declared value accurately, document your goods before loading, and understand exactly what your coverage covers. Whether you are moving a studio apartment or a five-bedroom home, we match your protection level to your actual risk. Request a personalized quote and get coverage guidance built around your move, not a generic checklist.

FAQ

What is moving insurance interstate?

Moving insurance interstate refers to the valuation coverage options that federal law requires all licensed interstate movers to offer. The two mandated options are Released Value Protection and Full Value Protection, which differ significantly in payout structure and cost.

Do I need moving insurance for an interstate move?

Released Value Protection is automatically included in every interstate move at no charge, but it pays only $0.60 per pound per item. If you own high-value or lightweight goods, upgrading to Full Value Protection or purchasing a third-party policy is strongly advisable.

How much does Full Value Protection cost?

Full Value Protection costs approximately 1% of your declared shipment value, though deductibles and minimum declared values vary by mover. For a $40,000 shipment, expect to pay roughly $400 for this coverage level.

What is the deadline for filing a moving damage claim?

Under the Carmack Amendment, claims must be filed within nine months of delivery in writing, with a specific dollar amount and supporting documentation. For concealed damage, written notice must be given within five days of delivery to preserve your rights.

Does homeowner’s insurance cover interstate moves?

Some homeowner’s and renter’s policies provide limited moving coverage, but most exclude transit periods, storage, and specific perils common to long-distance moves. Contact your insurer before moving day to confirm exactly what your policy covers and where the gaps are.