Most people assume their homeowner or renter insurance covers everything during a move. That’s rarely true. Moving insurance is specialized coverage designed to protect your belongings during transit from damage, theft, or loss caused by accidents or improper handling. Standard home policies often exclude damages caused by moving companies, leaving you vulnerable during long-distance relocations. Understanding what moving insurance covers, what it excludes, and how to choose the right protection ensures your valuables arrive safely at your new home without unexpected financial losses.

Table of Contents

- Key takeaways

- What moving insurance covers and excludes

- How moving insurance compares to homeowner and renter policies

- Special considerations for long-distance, interstate, and DIY moves

- How to choose and use moving insurance effectively

- Protect your move with AMB Moving Services

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| What moving insurance covers | Moving insurance protects belongings during transit from accidents theft fire and improper handling by professional movers. |

| Exclusions to note | It excludes damage to self packed boxes unless there is visible external damage to the container. |

| Homeowners vs moving | Homeowners or renters policies may cover some transit risks but do not typically cover damage caused by the moving company unless you add a rider. |

| Claims timelines | Claims require prompt documentation and meeting deadlines especially for interstate moves. |

| DIY and international moves | DIY and international relocations usually need special or third party insurance due to higher risks. |

What moving insurance covers and excludes

Moving insurance protects your belongings from specific perils during transportation. Coverage typically includes accidents, theft, fire, and improper handling by professional movers. If your furniture gets damaged when movers drop it down stairs or your electronics break during loading, these incidents fall under standard moving insurance protection. The policy responds when the moving company’s negligence or unavoidable accidents cause harm to your possessions.

Exclusions matter just as much as coverage. Moving insurance usually excludes damage to boxes you packed yourself unless there’s visible external damage to the container. If you pack your dishes and they break inside an undamaged box, the insurance won’t cover it. Acts of God like floods, earthquakes, or severe storms may also be excluded unless you purchase additional third-party coverage. Understanding these boundaries helps you avoid surprises when filing claims.

Perishable items, valuables like jewelry and cash, and extremely fragile collectibles often have limited or no coverage under standard policies. Moving companies typically exclude these high-risk items or offer minimal protection. Review your policy’s specific exclusions before your move and consider separate insurance for valuable items. Knowing your rights and responsibilities as a customer helps you navigate these limitations effectively.

Pro Tip: Take detailed photos of high-value items before packing and keep receipts or appraisals in a separate folder. This documentation becomes critical if you need to file a claim for damaged or lost belongings.

The distinction between covered and excluded items shapes how you prepare for your move. If you’re transporting family heirlooms or expensive electronics, ask your moving company about additional coverage options or purchase third-party insurance. Standard policies protect everyday household goods but may leave gaps for specialty items. Review the fine print and ask specific questions about items that matter most to you.

“Moving insurance bridges the gap between what movers are legally required to cover and what your belongings are actually worth. Without it, you’re gambling with your possessions.”

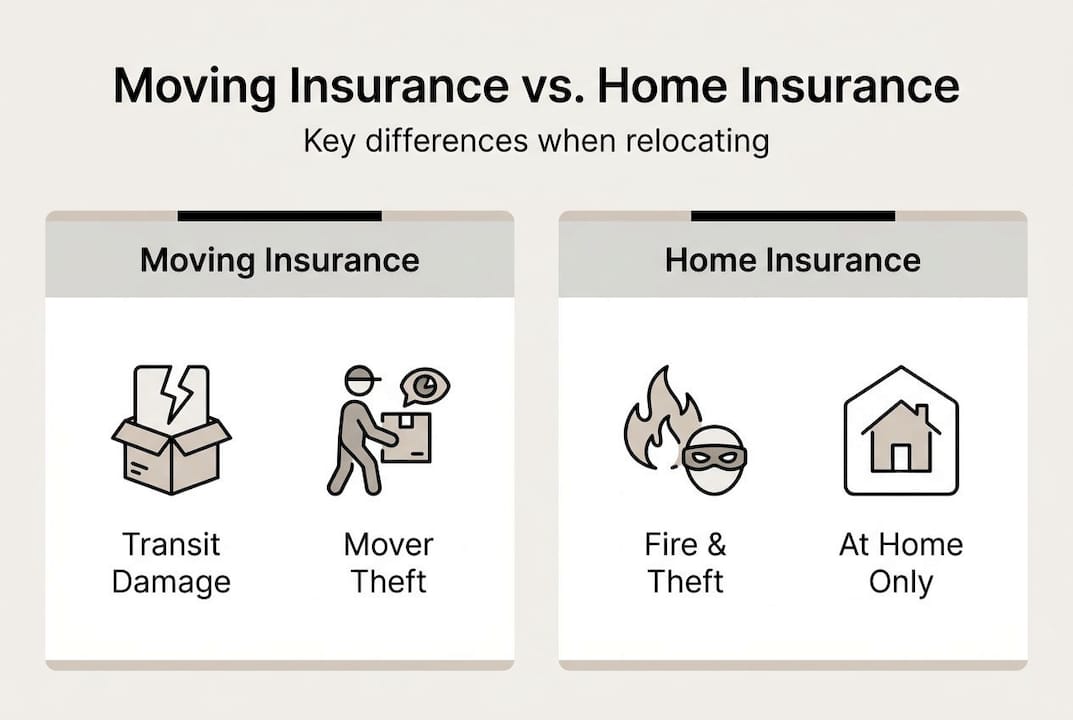

How moving insurance compares to homeowner and renter policies

Homeowners and renters insurance policies cover your belongings in many situations, but moving creates unique risks. These policies usually protect against perils like fire, theft, or water damage during transit. If your moving truck catches fire or gets stolen, your home insurance might cover the loss. However, damage caused by improper handling by movers is typically excluded without additional coverage.

The gap between home insurance and moving insurance centers on who causes the damage. Your homeowner policy protects against external threats but not the moving company’s mistakes. If movers drop your dresser and it breaks, or if they improperly secure items causing damage during transport, your home insurance won’t respond. Moving insurance specifically covers these handling-related damages that occur during the relocation process.

Some insurance companies offer riders or endorsements to extend coverage during moves. These add-ons can bridge the gap between your existing policy and moving-specific risks. You must add these proactively before your move, not after damage occurs. Contact your insurance agent weeks before moving day to discuss available options and costs. The rider might be more affordable than purchasing separate moving insurance.

| Coverage Type | Handles Transit Perils | Covers Mover Damage | Typical Cost |

|---|---|---|---|

| Homeowner/Renter Insurance | Yes (fire, theft) | Usually no | Included in existing premium |

| Home Insurance Rider | Yes | Sometimes | $50-$200 additional |

| Moving Company Insurance | Limited | Yes | Varies by valuation |

| Third-Party Moving Insurance | Yes | Yes | 1-4% of shipment value |

Moving insurance is designed specifically for transit and handling risks during relocation. It covers scenarios your home policy excludes and provides specialized claims processes for moving-related damages. Professional movers understand these policies and can explain coverage options based on your shipment’s value and distance. Always review both your existing policy and the moving company’s insurance options before deciding on protection levels.

Pro Tip: Call your home insurance agent at least three weeks before moving to understand exactly what your current policy covers during transit. This conversation reveals gaps and helps you make informed decisions about additional coverage.

Understanding moving cost considerations includes factoring in insurance expenses. While it adds to your budget, proper coverage prevents potentially devastating financial losses if damage occurs. Weigh the cost of insurance against the replacement value of your belongings and your financial ability to absorb losses.

Special considerations for long-distance, interstate, and DIY moves

Long-distance and interstate moves introduce stricter requirements and higher risks. Federal regulations require moving companies to offer basic liability coverage, but claims must be filed within 9 months for interstate moves. This deadline is firm. Missing it means losing your right to compensation regardless of how severe the damage. State-to-state moves fall under federal jurisdiction, creating different rules than local relocations.

Self-packed boxes present unique challenges for insurance coverage. Moving companies generally won’t cover damage to items you packed yourself unless the box shows obvious external damage. If you pack fragile items improperly and they break inside an intact box, you bear the loss. This exclusion protects movers from liability for packing mistakes they didn’t make. Professional packing services eliminate this gap by making the moving company responsible for proper packing and resulting damage.

DIY moves require completely different insurance approaches. When you rent a truck and move yourself, the moving company’s insurance doesn’t apply because there is no moving company. You need third-party insurance coverage to protect your belongings during a self-move. Rental truck companies offer basic coverage, but it’s often minimal. Consider purchasing separate moving insurance from specialized providers who cover DIY relocations.

- Document everything before the move with dated photos or videos of all items

- Create a detailed written inventory listing each item’s condition and estimated value

- Keep this documentation separate from your belongings in case boxes get lost

- Review federal and state claim deadlines based on your move type

- Understand the difference between released value and full value protection

- Purchase additional coverage for high-value items that exceed standard limits

International and cross-country moves carry higher risks due to longer transit times and more handling points. Items change hands multiple times, increasing damage potential. Weather exposure during multi-day transport adds risk. These factors make comprehensive insurance more valuable for long-haul moves. The small additional cost provides significant peace of mind when your belongings travel thousands of miles.

Pro Tip: For interstate moving projects, set a calendar reminder for eight months after delivery. This gives you one month before the nine-month claim deadline to address any issues you discover later.

| Move Type | Claim Deadline | Self-Pack Coverage | Recommended Insurance Level |

|---|---|---|---|

| Local (intrastate) | Varies by state | Usually excluded | Released value often sufficient |

| Interstate | 9 months federal | Excluded without external damage | Full value protection recommended |

| DIY/Self-Move | Policy dependent | Not applicable | Third-party comprehensive required |

| International | Varies by carrier | Usually excluded | Maximum coverage essential |

Verifying your moving company’s licensing helps ensure legitimate insurance coverage. Learn how to verify a licensed interstate moving company before signing contracts. Unlicensed movers may offer insurance that’s worthless when you need it. Federal registration and proper licensing indicate the company follows regulations and maintains required insurance standards.

How to choose and use moving insurance effectively

Choosing the right moving insurance starts with understanding your options. Released value coverage is the minimum required by law and costs nothing extra, but it only provides 60 cents per pound per item. A 50-pound television damaged beyond repair would net you just $30. Full value protection costs more but covers repair, replacement, or cash settlement at current market value. Third-party insurance from specialized providers offers the most comprehensive coverage and typically costs 1-4% of your shipment’s declared value.

Obtain a written contract detailing all insurance and valuation coverage terms before your move. Verbal promises mean nothing if damage occurs. The contract should specify the coverage type, deductibles, exclusions, and claims procedures. Read every section carefully and ask questions about unclear terms. This document becomes your primary evidence if you need to file a claim later.

Creating a detailed inventory protects you during claims. List every item being moved with its current condition and estimated value. Take photos or videos showing the condition of furniture, electronics, and valuable items before packing. Date these records and store copies separately from your shipment. If items arrive damaged, this documentation proves their pre-move condition and supports your claim value.

- Compare at least three coverage options: released value, full value, and third-party insurance

- Calculate your shipment’s total value honestly, including replacement costs for major items

- Review exclusions for high-value items like jewelry, art, or collectibles

- Ask about deductibles and how they affect claim payouts

- Confirm claim filing deadlines and required documentation

- Keep all insurance documents accessible during and after the move

Report damage immediately upon delivery. Don’t sign the delivery receipt without inspecting your belongings first. Note any visible damage on the receipt before the movers leave. Discovering hidden damage later is common, but documenting issues within 24 hours strengthens your claim. Take photos of damaged items and their packaging. Contact both the moving company and your insurance provider promptly to start the claims process.

Pro Tip: Consider professional packing services for fragile or valuable items. When movers pack your belongings, they assume liability for packing-related damage, eliminating a major coverage exclusion.

File claims according to deadlines specified in your contract and policy. Interstate moves require filing within nine months, but some policies have shorter windows. Missing deadlines voids your right to compensation regardless of damage severity. Keep copies of all claim correspondence and follow up regularly. Persistence pays off when dealing with insurance claims.

- Maintain a dedicated folder with your moving contract, insurance policy, inventory, and photos

- Use certified mail or email with read receipts when submitting claim documents

- Follow up weekly if you don’t receive claim status updates

- Escalate to supervisors if initial claim responses are unsatisfactory

- Consider state consumer protection agencies if legitimate claims are denied unfairly

Protect your move with AMB Moving Services

Navigating moving insurance complexities becomes simpler with experienced professionals guiding you. AMB Moving Services specializes in interstate and long-distance moving with comprehensive protection options tailored to your needs. Our team helps you understand coverage choices and select the right insurance level for your belongings’ value and your move’s distance.

Our professional packing services eliminate coverage gaps by ensuring proper packing and handling from start to finish. When we pack your items, we assume full responsibility for packing-related damage, giving you complete peace of mind. Trust our federally licensed team to guide you through a secure and well-insured moving experience. Explore our full range of moving services to find the perfect solution for your relocation.

Frequently asked questions

What exactly does moving insurance protect during my relocation?

Moving insurance covers damage to your belongings caused by accidents, theft, fire, or improper handling during transit. It typically excludes items you packed yourself unless external box damage is visible, and may not cover acts of God without additional third-party coverage.

Does my homeowner or renter insurance cover damages during a move?

Homeowner and renter policies usually cover perils like fire or theft during transit but exclude damage caused by movers’ improper handling. You may need to add a rider to your existing policy or purchase separate moving insurance to fill these gaps.

How do I file a moving insurance claim if my items get damaged?

Document all damage immediately with photos and note issues on the delivery receipt before movers leave. Contact your moving company and insurance provider within 24 hours, then file a formal claim with your inventory, photos, and damage documentation within the policy’s deadline, typically nine months for interstate moves.

What insurance do I need for a DIY or self-packed move?

DIY moves require third-party insurance since moving company policies don’t apply when you transport items yourself. Self-packed boxes in professional moves usually aren’t covered unless external damage is visible, so consider having movers pack fragile or valuable items to ensure coverage.

How do I choose between released value and full value protection?

Released value costs nothing but only pays 60 cents per pound, meaning a damaged 100-pound item nets you $60. Full value protection costs more but covers repair, replacement, or market value settlement. Choose based on your belongings’ total value and your financial ability to absorb potential losses.