Many people assume their moving company automatically covers every item during a cross-country relocation, only to discover too late that standard protection offers minimal compensation. Understanding relocation insurance is essential for anyone planning a long-distance move across the U.S. This guide clarifies what relocation insurance covers, explains your coverage options, breaks down cost factors, and shows you how to file claims if damage occurs. You’ll learn how to choose the right protection level to safeguard your belongings throughout the entire journey.

Table of Contents

- Key takeaways

- What is relocation insurance and why do you need it?

- Types of relocation insurance coverage

- How relocation insurance costs are determined and factors to consider

- How to file a claim and ensure your move stays protected

- Protect your move with trusted interstate relocation services

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Definition and purpose | Relocation insurance protects possessions during transport on long moves and acts as a financial safety net for items that are damaged, lost, or stolen. |

| Basic vs full coverage | Released value coverage is the default 60 cents per pound per item, while full value protection covers repair, replacement, or cash settlement for lost or damaged items. |

| Cost and risk factors | Deductibles and coverage limits affect how much you receive, and high value belongings benefit from enhanced protection. |

| Before you move | Review your homeowners or renters policy and compare with moving company options to choose coverage that aligns with item value and risk. |

What is relocation insurance and why do you need it?

Relocation insurance protects your possessions during transport when you move across state lines or long distances. Unlike homeowners insurance, which typically excludes items in transit, relocation insurance protects goods specifically while moving companies handle them. This coverage becomes your financial safety net if items arrive damaged, broken, or lost.

Most moving companies provide basic carrier liability automatically, but this default protection offers surprisingly limited compensation. Released value coverage, the industry standard minimum, typically pays only 60 cents per pound per item. That means your 50-pound flat-screen TV worth $1,200 would receive just $30 in compensation if damaged. For a 10-pound laptop valued at $2,000, you’d get only $6.

Long-distance moves increase exposure to potential damage through extended transport times, multiple handling points, and varied road conditions. Your belongings travel hundreds or thousands of miles, often spending days in a truck navigating highways, weather changes, and loading dock transfers. Each transition point creates opportunities for accidents, shifts in cargo, or mishandling.

Pro Tip: Review your homeowners or renters insurance policy before your move. Some policies offer limited coverage for items in transit, but most exclude moving-related damage entirely or cap coverage at minimal amounts.

Insurance options range from basic released value to full value protection that covers repair costs, replacement value, or cash settlements. Understanding coverage limits, deductibles, and exclusions helps you choose appropriate protection for your belongings’ actual value. High-value items like antiques, electronics, jewelry, or artwork particularly benefit from enhanced coverage since basic liability falls far short of replacement costs.

Key factors that make relocation insurance essential:

- Standard carrier liability provides minimal per-pound compensation

- Long-distance transport increases damage risk through extended handling

- Homeowners insurance rarely covers items during moves

- Full value protection offers comprehensive repair or replacement

- Coverage limits and deductibles significantly affect claim payments

Types of relocation insurance coverage

Moving companies offer several coverage options with vastly different protection levels and costs. Understanding each type helps you match coverage to your belongings’ value and your risk tolerance.

Released value coverage represents the most basic protection and comes included in your moving contract at no additional charge. This minimal liability option compensates you at 60 cents per pound per article, regardless of actual value. A damaged antique dresser weighing 200 pounds receives only $120, even if its market value exceeds $5,000. Federal regulations require movers to offer this baseline coverage, but it rarely provides adequate compensation for modern household goods.

Full value protection offers comprehensive coverage where the moving company assumes liability for the replacement value of lost or damaged items. Under this option, movers must either repair the item, replace it with comparable goods, or provide a cash settlement for current market value. Deductibles typically apply, ranging from zero to several hundred dollars depending on your policy terms and premium costs. This coverage protects your belongings at their actual worth rather than arbitrary per-pound calculations.

Third-party insurance provides an alternative to mover-provided coverage through independent insurance companies. These policies can supplement or replace carrier liability, offering customized protection levels, broader coverage terms, and sometimes lower premiums. Third-party insurers specialize in moving protection and may cover items that movers exclude, such as jewelry, important documents, or collectibles.

Pro Tip: Request written documentation of all coverage terms, exclusions, and claim procedures before signing your moving contract. Understanding exactly what your policy covers prevents surprises if you need to file a claim.

| Coverage Type | Protection Level | Cost | Best For |

|---|---|---|---|

| Released Value | 60 cents/pound | Included | Minimal belongings or tight budgets |

| Full Value Protection | Repair/replacement at market value | Additional premium | Standard household goods |

| Third-Party Insurance | Customizable coverage limits | Varies by provider | High-value items or specialized needs |

Coverage limits and deductibles directly impact claim amounts you receive. A $500 deductible means you pay the first $500 of any claim before insurance coverage begins. Higher deductibles reduce premium costs but increase out-of-pocket expenses if damage occurs. Maximum coverage limits cap total claim payments, so declaring accurate inventory values ensures adequate protection.

Reading policy details thoroughly reveals important exclusions and limitations. Most policies exclude:

- Items you pack yourself rather than professional packing services

- Damage from inherent vice or pre-existing conditions

- Perishable goods or plants

- Cash, securities, or important documents

- Damage discovered after signing delivery paperwork

Understanding these distinctions helps you choose between basic carrier liability, enhanced moving services coverage, or third-party policies. Match your coverage selection to your belongings’ total value and replacement costs rather than accepting default minimum protection.

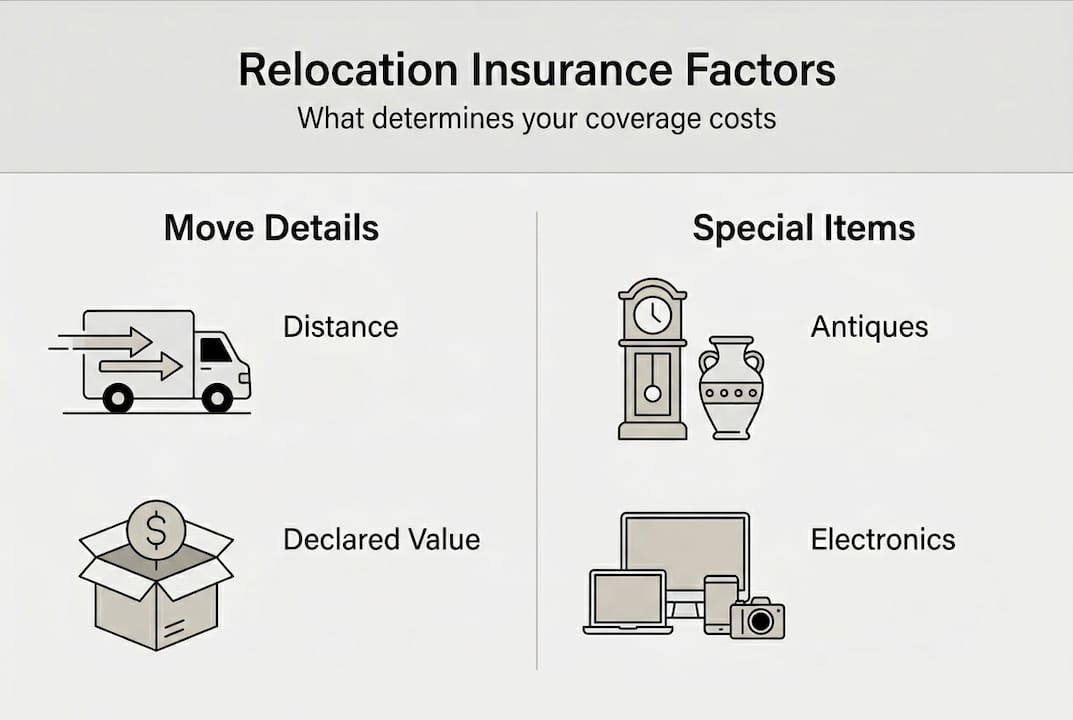

How relocation insurance costs are determined and factors to consider

Insurance pricing for long-distance moves depends on multiple variables that reflect risk levels and coverage scope. Understanding these factors helps you budget accurately and identify opportunities to manage costs.

Declared value represents the foundation of insurance pricing. You estimate your belongings’ total worth, and insurers calculate premiums as a percentage of that declared amount. Full value protection typically costs $1 to $2 per $100 of declared value, though rates vary by carrier and coverage terms. A household inventory valued at $50,000 might cost $500 to $1,000 for comprehensive coverage, while released value liability comes included at no extra charge.

Distance and route characteristics affect premium calculations because longer moves expose belongings to extended transport time and more handling. Cross-country relocations from New York to California face higher rates than shorter interstate moves. Routes through mountainous terrain, areas with extreme weather, or regions with higher accident rates may increase premiums due to elevated risk factors.

Inventory completeness and accuracy directly impact both coverage adequacy and claim processing. Detailed inventories listing each item’s description, age, condition, and estimated value provide documentation for claims and help insurers assess appropriate premium levels. Vague or incomplete inventories lead to disputes during claims and may result in reduced settlements.

Factors influencing relocation insurance costs:

- Total declared value of household goods

- Coverage type selected (released value, full value, or third-party)

- Distance and route complexity of your move

- Deductible amount chosen

- Special handling requirements for high-value items

- Moving company’s claims history and insurance carrier

Deductibles offer a direct trade-off between upfront premium costs and potential out-of-pocket expenses. Choosing a $250 deductible instead of zero deductible reduces your premium by 10% to 20%, but you’ll pay the first $250 of any claim yourself. Evaluate your risk tolerance and emergency fund capacity when selecting deductible levels.

Steps to optimize your insurance costs:

- Create a detailed inventory with photos and estimated values for all belongings

- Request quotes from multiple moving companies and third-party insurers

- Compare coverage terms, exclusions, and deductibles across all options

- Consider higher deductibles if you have emergency savings to cover initial claim costs

- Ask about discounts for professional packing or additional protective services

- Review and adjust declared values to match actual replacement costs

Comparison shopping proves essential because rates and coverage terms vary significantly among providers. Some moving cost factors include carrier reputation, claims processing efficiency, and policy flexibility. Request written quotes detailing coverage limits, deductibles, exclusions, and premium costs to make informed comparisons.

Special items like antiques, artwork, pianos, or electronics may require separate valuation and additional premium charges. High-value items exceeding standard coverage limits need declared separately with supporting documentation such as appraisals or purchase receipts. This extra step ensures adequate protection for irreplaceable or expensive possessions.

How to file a claim and ensure your move stays protected

Filing a successful relocation insurance claim requires prompt action, thorough documentation, and clear communication with your moving company and insurer. Following proper claims processes maximizes your chances of fair compensation.

Before moving day, create a detailed inventory documenting every item’s condition. Photograph or video record furniture, electronics, and valuable possessions from multiple angles. Note existing scratches, dents, or wear in your inventory list. This pre-move documentation establishes baseline condition and proves damage occurred during transport rather than beforehand.

Pro Tip: Use your smartphone to create a digital inventory with timestamped photos. Cloud storage ensures you won’t lose documentation even if your devices get damaged or lost during the move.

Inspect your belongings carefully during delivery before signing any paperwork. Check furniture for new damage, test electronics to verify functionality, and examine boxes for crushing or water damage. Document every problem immediately with photos and written notes. Your signature on the delivery receipt acknowledges acceptance, so thoroughly inspect everything before signing.

“Clear documentation at delivery time is your strongest protection. Never sign paperwork stating everything arrived in good condition until you’ve actually verified it.” — Federal Motor Carrier Safety Administration

Contact your moving company and insurance provider within 24 hours of discovering damage. Most policies require prompt notification, with specific deadlines ranging from immediate reporting to 30 days after delivery. Delayed reporting can jeopardize your claim or reduce settlement amounts. Provide your inventory documentation, delivery receipts, and damage photos during initial contact.

Steps to file your relocation insurance claim:

- Document all damage with detailed photos from multiple angles immediately upon discovery

- Note damaged items on the delivery receipt before signing, or write “subject to inspection” if you need time

- Contact your moving company’s claims department within 24 hours

- Notify your insurance provider simultaneously if you purchased third-party coverage

- Complete all required claim forms thoroughly with specific damage descriptions

- Submit supporting documentation including inventory lists, photos, receipts, and appraisals

- Keep copies of all correspondence, forms, and evidence for your records

- Follow up regularly on claim status and respond promptly to any information requests

- Review settlement offers carefully and negotiate if compensation seems inadequate

- Understand your rights under federal regulations and state laws governing moving claims

Follow your insurer’s specific claim forms and documentation requirements precisely. Missing information or incomplete submissions delay processing and may result in claim denials. Provide repair estimates from qualified professionals for damaged items, or replacement cost documentation for destroyed belongings. Original purchase receipts, appraisals, or comparable item listings support your claimed values.

Keep copies of every document you submit and all correspondence you receive. Maintain a claim file with dates, names of representatives you speak with, and summaries of conversations. This organized record proves invaluable if disputes arise or you need to escalate your claim to supervisors or regulatory agencies.

Understanding your rights and responsibilities as a moving customer helps you navigate the claims process effectively. Federal regulations require interstate movers to acknowledge claims within 30 days and provide settlement offers or denial explanations within 120 days. If you disagree with a settlement offer, you can negotiate, request additional review, or pursue dispute resolution through regulatory agencies.

Working with licensed interstate moving companies provides additional consumer protections and clearer claim procedures. Reputable carriers maintain established claims departments, transparent processes, and fair settlement practices that simplify resolution when damage occurs.

Protect your move with trusted interstate relocation services

Planning a long-distance move requires more than just packing boxes and loading trucks. Professional interstate moving services combine experienced handling, comprehensive insurance options, and transparent pricing to protect your belongings throughout the journey. AMB Moving & Storage Inc. specializes in cross-country relocations backed by federal licensing, full value protection options, and dedicated customer support.

Our long-distance moving solutions include detailed inventory documentation, secure packing materials, and careful loading techniques that minimize damage risk. We work with you to select appropriate insurance coverage matching your belongings’ value and your budget. From initial consultation through final delivery, our team handles logistics while you focus on settling into your new home. Professional packing services ensure fragile items receive proper protection and qualify for full insurance coverage.

Frequently asked questions

What is relocation insurance?

Relocation insurance protects your belongings from damage or loss during a move. It supplements or replaces the minimal standard liability coverage moving companies provide automatically. This specialized protection covers items specifically while in transit, filling the gap left by homeowners insurance policies that typically exclude moving-related damage.

Does my moving company automatically provide relocation insurance?

Moving companies provide basic released value coverage automatically, but this minimal protection pays only 60 cents per pound regardless of actual item value. Adequate protection requires purchasing additional full value coverage or third-party insurance. Review your moving company insurance responsibilities carefully before assuming you have comprehensive protection.

How do I file a relocation insurance claim if something gets damaged?

Document damage immediately with photos and written notes during delivery. Notify both your moving company and insurer within 24 hours of discovering problems. Submit required claim forms with supporting evidence including inventory lists, damage photos, and repair estimates. Follow the detailed steps for filing a moving insurance claim to ensure proper processing.

How much does full value protection cost for a long-distance move?

Full value protection typically costs $1 to $2 per $100 of declared value. A household inventory worth $50,000 would cost approximately $500 to $1,000 for comprehensive coverage. Actual rates vary based on distance, route, deductible selection, and your moving company’s insurance carrier.

Can I use my homeowners insurance instead of buying relocation coverage?

Most homeowners insurance policies exclude items in transit or provide only minimal coverage during moves. Review your policy carefully and contact your insurance agent to verify moving-related protection. In most cases, purchasing dedicated relocation insurance offers significantly better coverage than relying on homeowners policies.